Orphan Client in the Philippines: How to Find a New Financial Advisor and What to Expect

This guide explains what it means to be an orphan client in the Philippines, what happens to your insurance or investments when your advisor is no longer available, and how to choose a licensed financial advisor who can properly take over your account. Learn the exact transition process, what to expect in the first 90 days, and how to avoid costly mistakes before making your next decision.

FINANCIAL LITERACY

David Isaiah Angway RFP

1/30/20264 min read

I want to change a Financial advisor

If you lost your financial advisor and suddenly do not know who to call, you are not alone.

In the Philippines, this happens more often than people admit, and it puts your money at risk if overlooked.

Table of Contents

What an orphan client really means

Why financial advisors disappear

What happens to your policy when your advisor is gone

How to choose a new financial advisor properly

What the transition process looks like in the Philippines

What you should expect in the first 90 days

TL;DR

An orphan client is someone whose financial advisor can no longer service their policy. Your policy does not disappear; service simply slows down or stops. You need a licensed, active advisor who can formally take over servicing. The right transition includes review, documentation, and clear expectations, not pressure to buy something new.

What an orphan client really means

In the Philippine financial system, most insurance and investment products are serviced by agents. This means your policy is tied to a company, but the day-to-day servicing is handled by an individual advisor.

You become an orphan client when that advisor can no longer legally or practically assist you.

Your policy still exists. Your premiums are still valid. Your benefits are still intact.

What is missing is accountability.

Without an assigned advisor, tasks like claims assistance, fund switches, beneficiary updates, and annual reviews become slower and harder. Some clients only realize this problem when they urgently need help.

Why financial advisors disappear

There are four common reasons this happens in the Philippines.

First, career changes. Many advisors leave the industry, migrate abroad, or shift to corporate roles. Once their license or contract ends, they cannot service your policy.

Second, termination. Advisors who fail to meet maintenance requirements can lose their contract. This is more common than clients think, especially among part-time agents.

Third, retirement or death. If the advisor is not part of a team or does not plan succession, clients are left unattended.

Fourth, company transfer. Insurance Commission rules allow an advisor to represent only one life insurance company at a time. If your advisor moves companies, they cannot touch your existing policy.

What happens to your policy when your advisor is gone?

This is the part many clients misunderstand.

Your policy does not expire because your advisor left. The insurance company is still responsible for honoring valid claims.

However, without an assigned servicing advisor:

Claims may take longer due to incomplete documentation.

Policy changes require more back-and-forth with customer service.

No one proactively reviews your coverage or fund performance.

You are more likely to miss red flags like underinsurance or policy lapse risk.

In practice, orphan clients experience more friction and less clarity.

How to choose a new financial advisor properly

This decision matters more now than when you first bought insurance.

Start with licensing. Your new advisor should be active and licensed with the Insurance Commission. If investments are involved, look for SEC registration. If bank products are discussed, familiarity with the BSP matters.

Next, experience. Ask how long they have been practicing and how many active clients they serve today. Someone supervising 20 to 30 families is different from someone managing 300 with a support team.

Then, the scope of advice. If you now have dependents, businesses, or estate concerns, you need someone who can explain insurance beyond the basics.

Finally, temperament. You are not shopping for a salesperson. You are choosing someone who can explain calmly, document properly, and follow through.

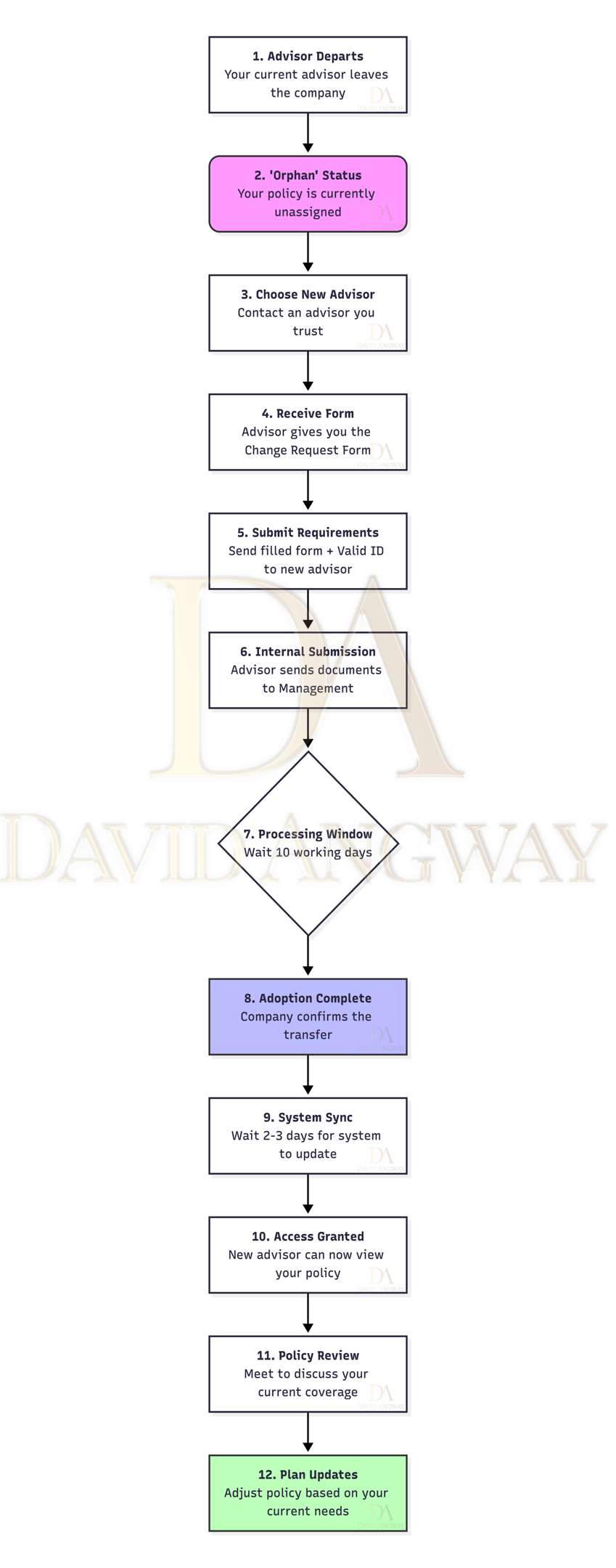

What the transition process looks like in the Philippines

For most insurers, the process includes:

A formal request to assign a new servicing advisor

Verification of your identity and policy ownership

A policy assessment session, usually 60 to 90 minutes

Documentation certifying the advisor assignment

This does not automatically mean buying a new product.

A proper advisor will first understand what you already have, what works, and what no longer fits.

What you should expect in the first 90 days

A professional transition usually looks like this.

Month one focuses on discovery. Your advisor reviews policies, beneficiaries, premium schedules, and fund allocation.

The second month addresses gaps. This might include updating beneficiaries, correcting outdated information, or explaining charges and risks you were never told about.

Month three sets direction. You agree on review frequency, communication expectations, and long-term planning priorities.

If your first meeting is purely about selling, that is a warning sign.

Common mistakes orphan clients make

The most common mistake is inaction. Clients delay for years until a claim or emergency forces the issue.

The second mistake is chasing familiarity. Choosing a friend or relative who is newly licensed may feel comfortable, but comfort does not replace competence.

The third mistake is product hopping. Some clients are unnecessarily convinced to replace policies, resulting in higher costs and reset charges.

A calm next step

If you are an orphan client, your priority is not buying something new. Your priority is restoring stewardship.

Find someone who treats your existing money with respect. Ask clear questions. Expect clear answers.

Good financial advice feels steady. It does not rush you. It does not confuse you. It makes you feel more in control after every conversation.

That is what you should expect this time.

For Sun Life Financial Client, I recommend you to download the form below for you to fill out and send it to your preferred advisor that can take care of you.

© 2026 David Angway