When Not to Surrender Your Insurance Policy in the Philippines (VUL and Life Insurance Guide)

Thinking of surrendering your VUL or life insurance because the premium feels heavy or the fund value is down? This guide for Filipino professionals and young families explains when you should not surrender, especially if you have dependents, debt, or no emergency fund. It includes a simple 30-minute policy check and safer ways to reduce costs without losing protection. Written from an estate planning perspective, focused on keeping your family financially stable when life happens.

INSURANCE PLANNINGESTATE PLANNING

David Isaiah Angway RFP

12/23/20256 min read

If you’re thinking about giving up your policy because money is tight, you’re not alone. I talk to many professionals, especially women, who balance work, family, and finances. The premium can feel like one more thing to worry about.

Before you decide to surrender, take a moment to review your options. Giving up your policy is permanent.

Getting coverage again later could cost more than you save now.

TL;DR

Main point: Only give up your policy if you can replace the coverage you lost right away. Make sure there’s no gap in your protection.

My advice: Only surrender if you already have new coverage in place and have saved three to six months' worth of expenses in an emergency fund.

To calculate this, add up your essential monthly expenses, such as rent, utilities, groceries, transportation, and debt payments.

Multiply this total by three to six, depending on how stable your income is. This amount will provide a financial cushion if you face unexpected events.

Quick answer

If giving up your policy means losing protection and you don’t have a new policy ready, don’t rush your decision.

If something happens to you next month, here’s the practical question to ask:

Will your family have enough money quickly, without needing to borrow or sell things in a hurry?

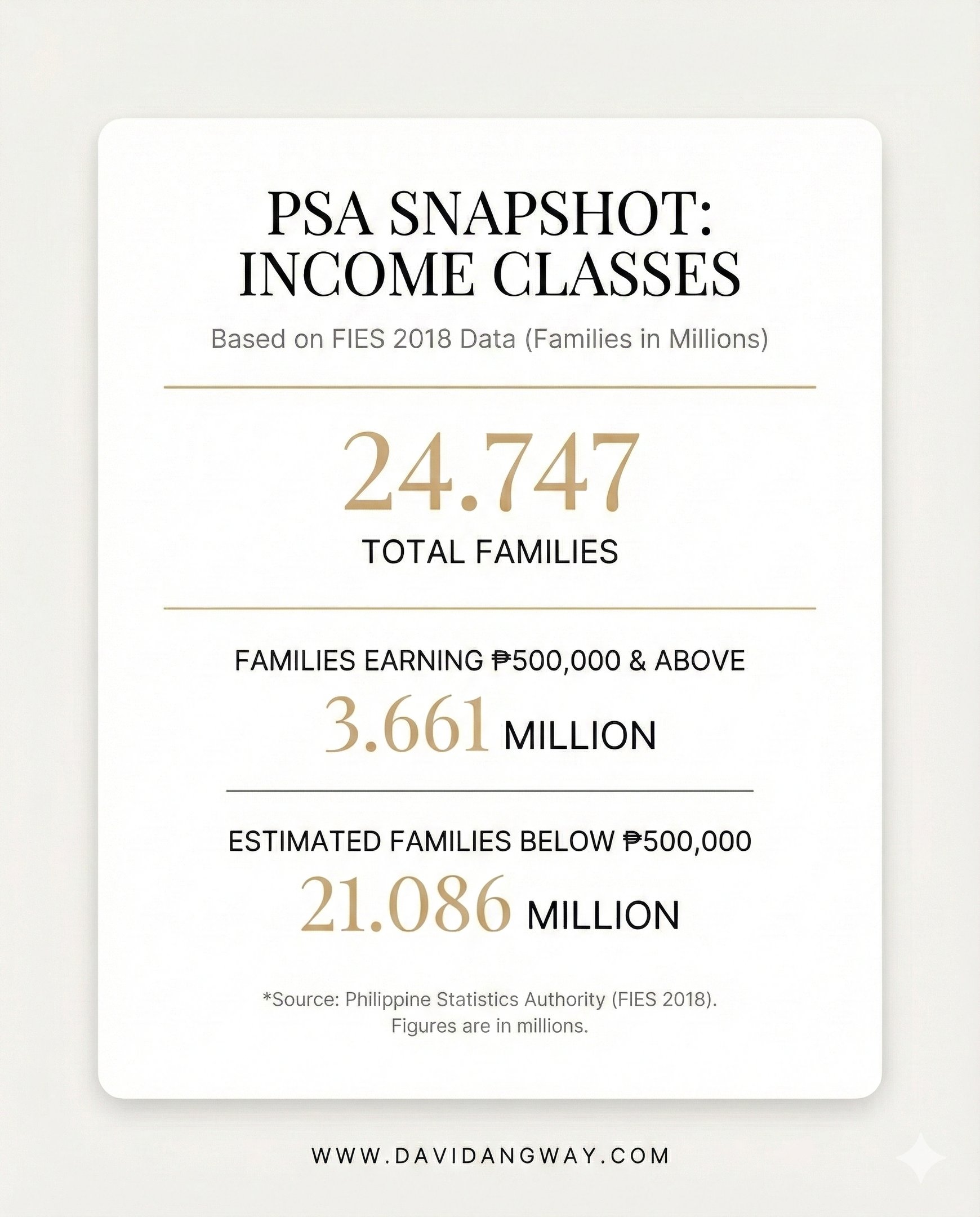

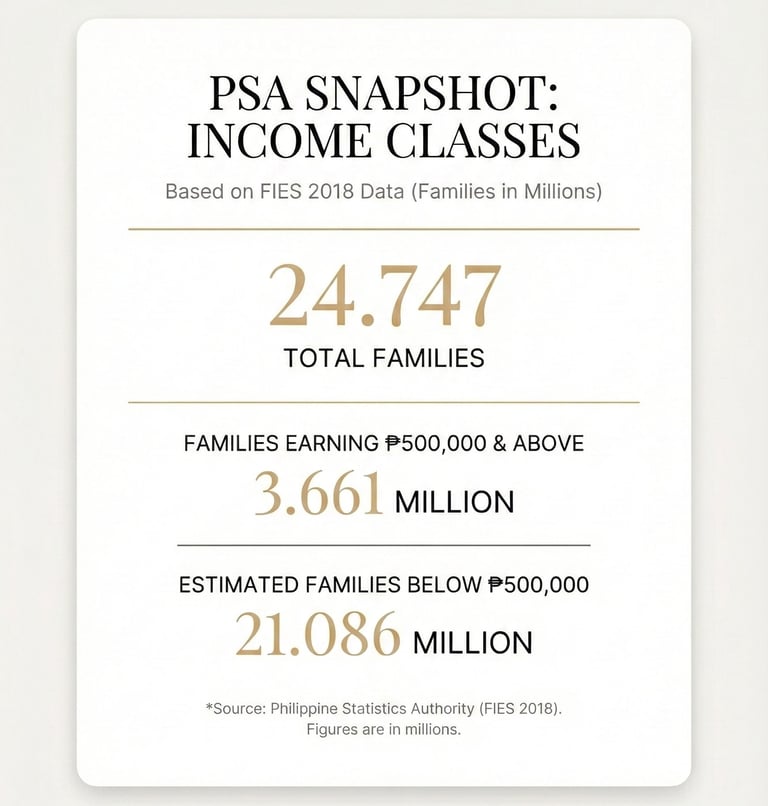

Footnote: PSA figures cited refer to annual family income (households), not individual salaries, based on the Philippine Statistics Authority’s Family Income and Expenditure Survey (FIES) 2018 income-class table (income class: ₱500,000 and over).

The real reason people regret surrendering

If you are earning 500,000 or less, this article most probably suits you

Most people surrender because of one stressful moment:

A big bill arrives.

The VUL fund value looks down.

The premium feels heavy.

You feel like you are paying but “not getting anything.”

Let me say this clearly, without any judgment.

Feeling overwhelmed doesn’t mean you’ve failed.

It means your plan might need a review, not a quick exit.

When you surrender, you may lose:

Your life coverage and riders you still need

Your underwriting terms from when you were younger and healthier

The ability to get the same coverage at the exact cost

The protection your family can claim quickly if something happens to you

If you own property, keep this in mind.

Property is valuable, but it’s not easy to turn into cash quickly. Your family might have assets but still struggle to pay urgent bills.

Ten situations when you usually shouldn’t surrender your policy.

1. You still have dependents.

If your spouse, child, or parent relies on you, surrendering can remove their only safety net.

Here’s a simple check: If your family would need at least a year of your income to get back on their feet, you still need coverage.

2. You have debt or long-term commitments.

Housing loan, car loan, business obligations, personal loans with co-makers, and tuition commitments.

If something happens to you, debts remain. Insurance protects your family from the need to borrow urgently or sell assets.

3. You do not have an emergency fund yet.

If you cash out your policy but don’t have an emergency fund, everyday expenses will likely use up that money quickly.

Target:

3 months of essentials if income is stable

6 months if income is variable or you support an extended family

4. Your policy is your only personal coverage.

Group life insurance through work is helpful, but it is usually not enough and ends when you leave the company.

Applying for new coverage isn’t the same as having it approved. Don’t surrender your policy until your replacement is active.

5. Your health has changed since you bought the plan.

Even controlled or mild issues can raise costs or affect approval: high blood pressure, elevated sugar, high cholesterol, fatty liver, weight gain, new maintenance meds, and recent hospital checks.

If your health has changed, don’t give up your policy quickly. You might not be able to get the same coverage at the same price.

6. You are surrendering mainly because your VUL fund value is down.

If your fund value is down, surrendering can make that loss permanent. A lower fund value means it’s time to review, not surrender right away.

Often, the real issue is structure: heavy riders, fund allocation that does not match your risk tolerance, or a premium level that is not sustainable.

7. You are still in the early years of the policy.

Many policies have higher charges in the first few years. If you surrender early, you might leave just after paying the most expensive part.

8. You will use the surrender value for non-essential spending.

Travel, gadgets, renovations that are not urgent, helping someone without a clear repayment plan, or a business idea that is not yet tested.

This is usually a costly trade-off: giving up long-term protection for your family for short-term spending.

9. You have property, and your family will need liquidity.

This is an estate planning detail that many families overlook.

When you pass away, your heirs need cash first. Hospital bills, funeral and settlement costs, property upkeep, loan payments, and living expenses do not wait.

Without enough cash, families may have to sell things quickly, borrow money, or even face disagreements.

10. You have no clear replacement plan.

Some people say, “I’ll just invest the money instead.” That can work only if you already have protection and the discipline to invest monthly for years.

For most families earning less than ₱500,000 a year, the safer order is to build your emergency fund first, get affordable protection, pay off high-interest debt, and then invest regularly.

MINI TAKEAWAY

If your plan feels overwhelming, it doesn’t mean you should surrender.

It often means you need a review and a setup you can keep up with comfortably.

Here’s a 30-minute policy check you can do this week.

Step 1. Know your monthly essentials

Write down your rent or mortgage, utilities, food, transportation, tuition, and debt payments.

Step 2. Set your emergency fund target

Multiply your monthly essentials by three or six, depending on how stable your income is.

Step 3. List your dependents and obligations

If you have anyone depending on you or any obligations, you still need coverage.

Step 4. Identify what your policy is doing today

Life coverage amount

Riders and benefits

Premium amount

If you have a VUL, check your fund allocation and whether your policy is sustainable long-term.

Step 5. If you are considering surrender, check the replacement first

If you still need insurance, make sure you have new coverage in place before you surrender your current policy.

Better options if your premium is heavy

If your premium feels too high, you usually have options before giving up your policy:

Reduce the number of riders who are no longer essential.

Adjust coverage to match what you can realistically maintain.

Change your premium schedule to something more manageable.

If you have a VUL, review your fund choices and make sure your policy can last long term.

If your goal is pure coverage, consider moving to a simpler protection plan.

Remember, your goal isn’t to keep a policy no matter what.

It’s to make sure your family is protected while you work toward financial security.

When surrendering can be reasonable.

It can make sense to surrender your policy if these things are true:

You have no dependents, and no one relies on your income. (Walang iiyak)

You already have an emergency fund that is 10x your annual income

You have no major debt that can pressure your family. (No more amortization, car, house and business loans)

You already have replacement coverage approved and active. If you still need insurance.

The policy structure is clearly mismatched, and alternatives have been reviewed.

If you’re unsure, don’t decide when you’re stressed.

Take time to review your options, then make your choice calmly.

If you feel like an “orphan” policyholder and no longer have an advisor to guide you,

I can help.

Send an inquiry for a quick policy review call. We’ll go through your coverage, costs, and next best step, clearly and without pressure.

What to read next

Protecting Family Wealth: Estate Planning Strategies to Prevent Sibling Conflict and Financial Mismanagement

Beneficiaries in the Philippines, the most common mistakes that delay claims and create family conflict

Digital Estate planning basics for young families: the simple documents and steps to protect your child and your assets

© 2026 David Angway