How to Stop Subscription Creep in the Philippines and Turn ₱60,000 a Year Into Investments

Are unused subscriptions quietly draining your money? Learn how the ₱400 GCash Rule helped stop subscription creep, save ₱60,000 per year, and turn small monthly charges into long-term investment growth in the Philippines.

FINANCIAL LITERACY

David Isaiah Angway

2/4/20265 min read

Last week, I received a bank notification:

“Your account balance is below the minimum.”

I froze.

Not because of one big purchase.

But because of small ones I forgot about.

If you’ve ever opened your bank app and thought, “Wait… what is this charge?” this is for you.

In this article, I’ll show you:

• How subscriptions quietly drain your money

• The simple GCash system that stopped mine

• How I redirected ₱60,000 into investments instead

• What that money could become in 5 years

TL;DR (If You’re in a Hurry)

Subscriptions feel small.

But mine cost me ₱60,000 in one year.

I fixed it by:

• Routing all subscriptions to GCash

• Keeping the balance under ₱400

• Letting payments fail if they weren’t essential

• Investing the recovered money annually

Result: Financial clarity and redirected capital.

Now let’s unpack it properly.

1. The Hidden Subscription Trap

Streaming.

Cloud storage.

Apps.

Online tools.

Premium upgrades.

Each one is ₱149. ₱299. ₱499.

Individually harmless.

Collectively expensive.

Online businesses design pricing to feel “small enough not to question.” That’s behavioral pricing strategy.

In the Philippines, Netflix remains the top digital streaming platform, according to Philstar. Competition from HBO, Apple TV+, and others continues to grow. That means more monthly charges competing for your wallet.

The danger is not the price.

It’s the automation.

2. Why You Feel Forced to Keep Paying

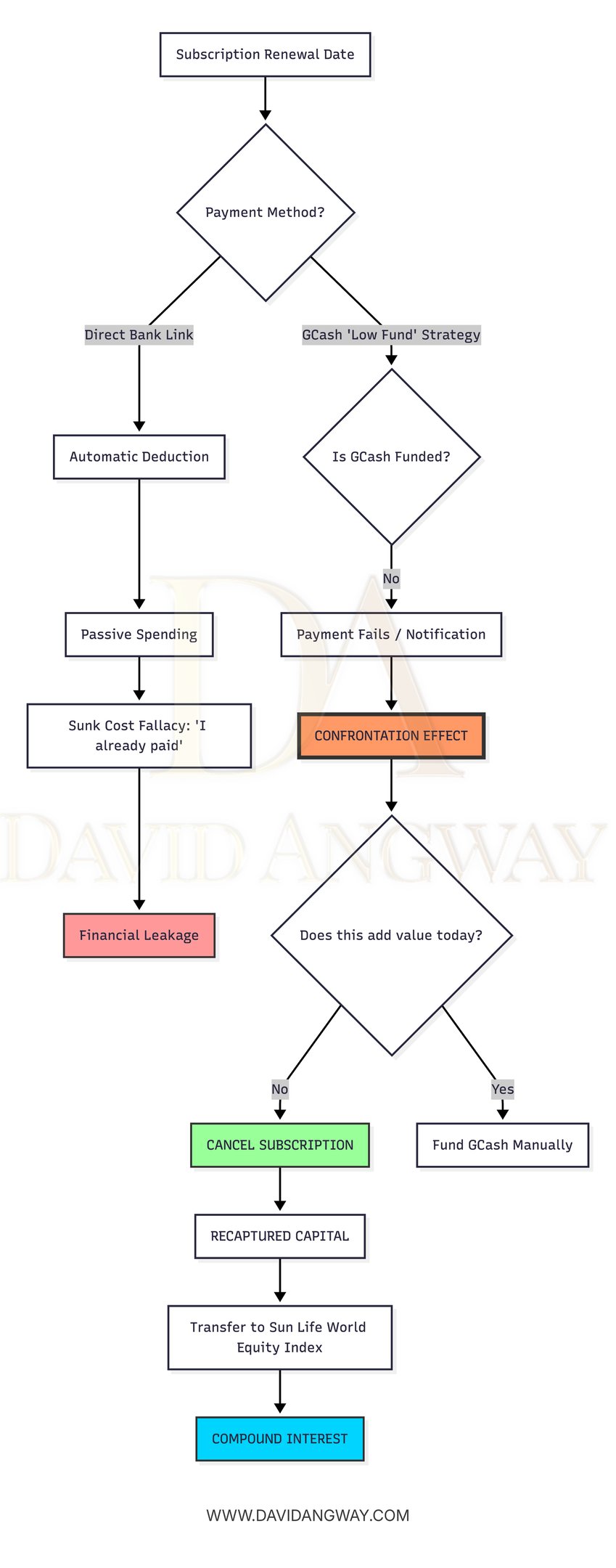

This is called the sunk cost fallacy.

You already paid.

So you feel obligated to use it.

You keep the gym membership.

You keep the streaming service.

You keep the cloud storage.

Even if you don’t use them.

The psychology is simple:

“I already spent money. Sayang.”

But financially, the past expense is irrelevant.

The only question that matters is:

Would you subscribe again today at full price?

If the answer is no, cancel it.

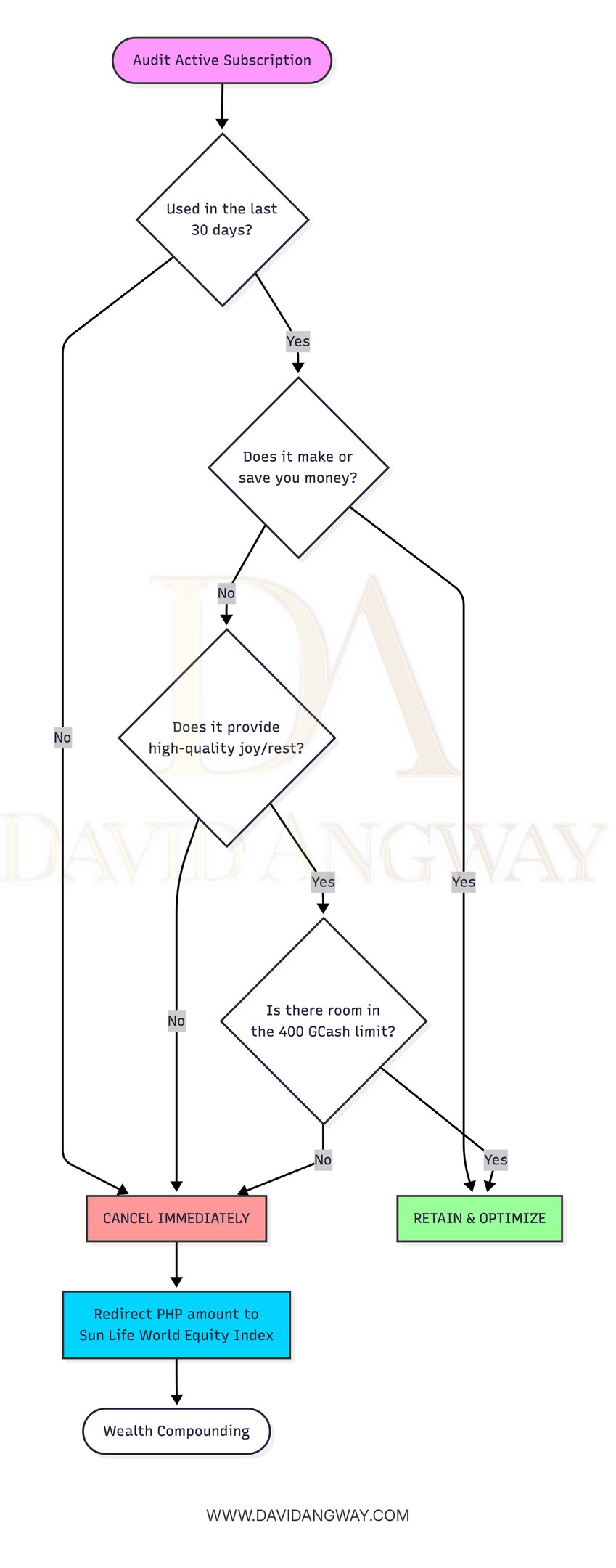

3. The ₱400 GCash Rule

Here’s what changed everything for me.

All subscriptions go to GCash.

Then I intentionally keep the balance below ₱400.

Why ₱400?

Because most streaming services fall below that threshold.

If the balance is insufficient, the payment fails.

That failure creates friction.

And friction in personal finance is powerful.

Instead of money silently leaving your bank account, you receive a visible notification.

Now you must decide:

Do I really want to fund this?

That moment is what I call the confrontation effect.

It forces clarity.

Important: Disable Auto-Cash In from your bank.

If GCash automatically tops up, the system collapses.

4. The One-Month Rule

Here’s the rule I follow:

If a payment fails and I don’t fund it within 48 hours, I cancel the subscription.

No emotional debates.

No overthinking.

If I truly need it, I will feel the inconvenience immediately.

If I don’t, it disappears quietly.

You can always resubscribe.

That flexibility removes fear.

5. What ₱60,000 Actually Means

Tracking my subscriptions for one year saved me approximately ₱60,000.

That’s ₱5,000 per month.

To give context:

• That’s several months of rent contribution in Metro Manila

• That’s school tuition support

• That’s investment capital

The issue is not lifestyle.

It’s leakage.

And leakage compounds.

6. What Happens If You Invest It Instead?

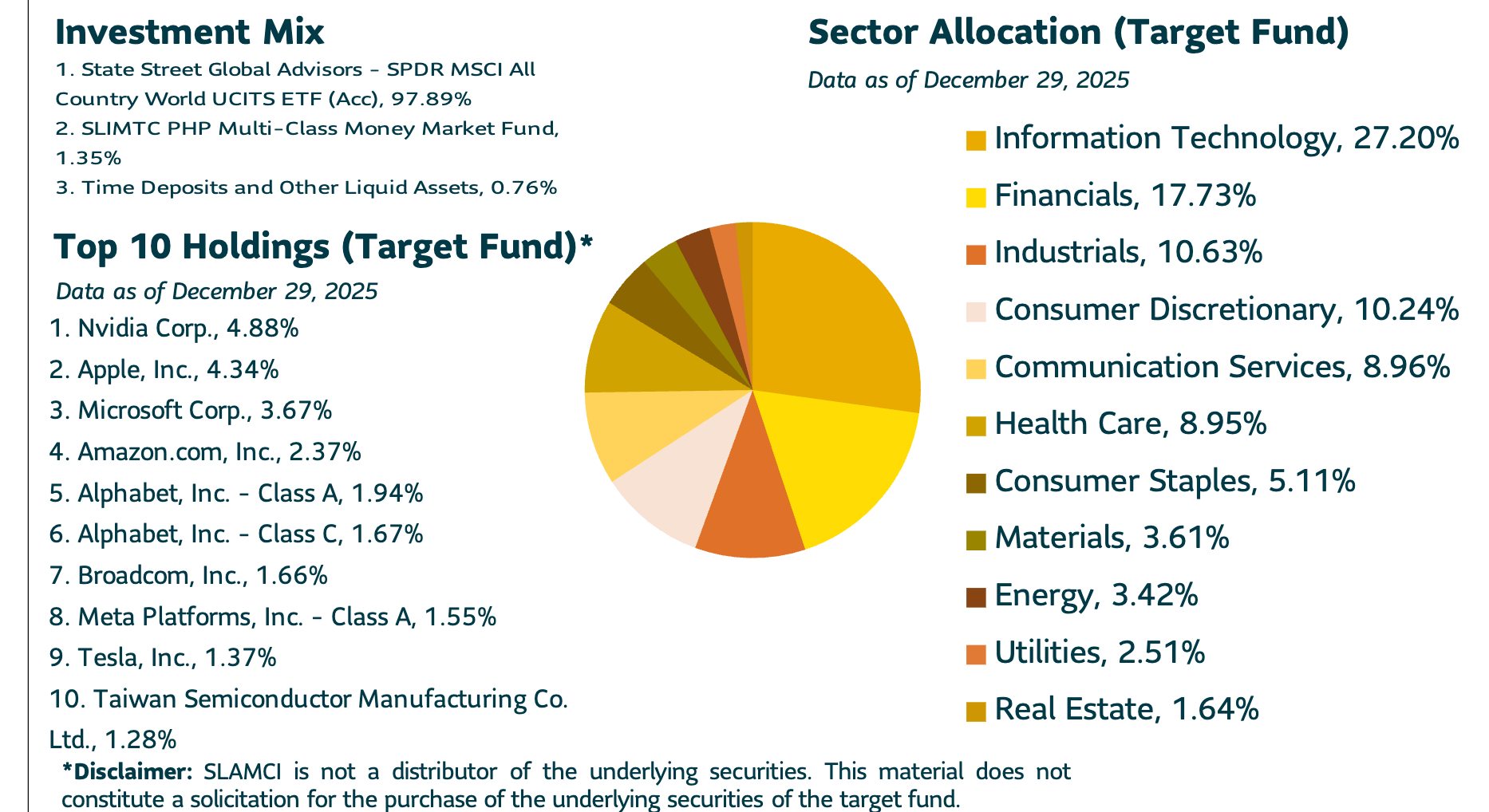

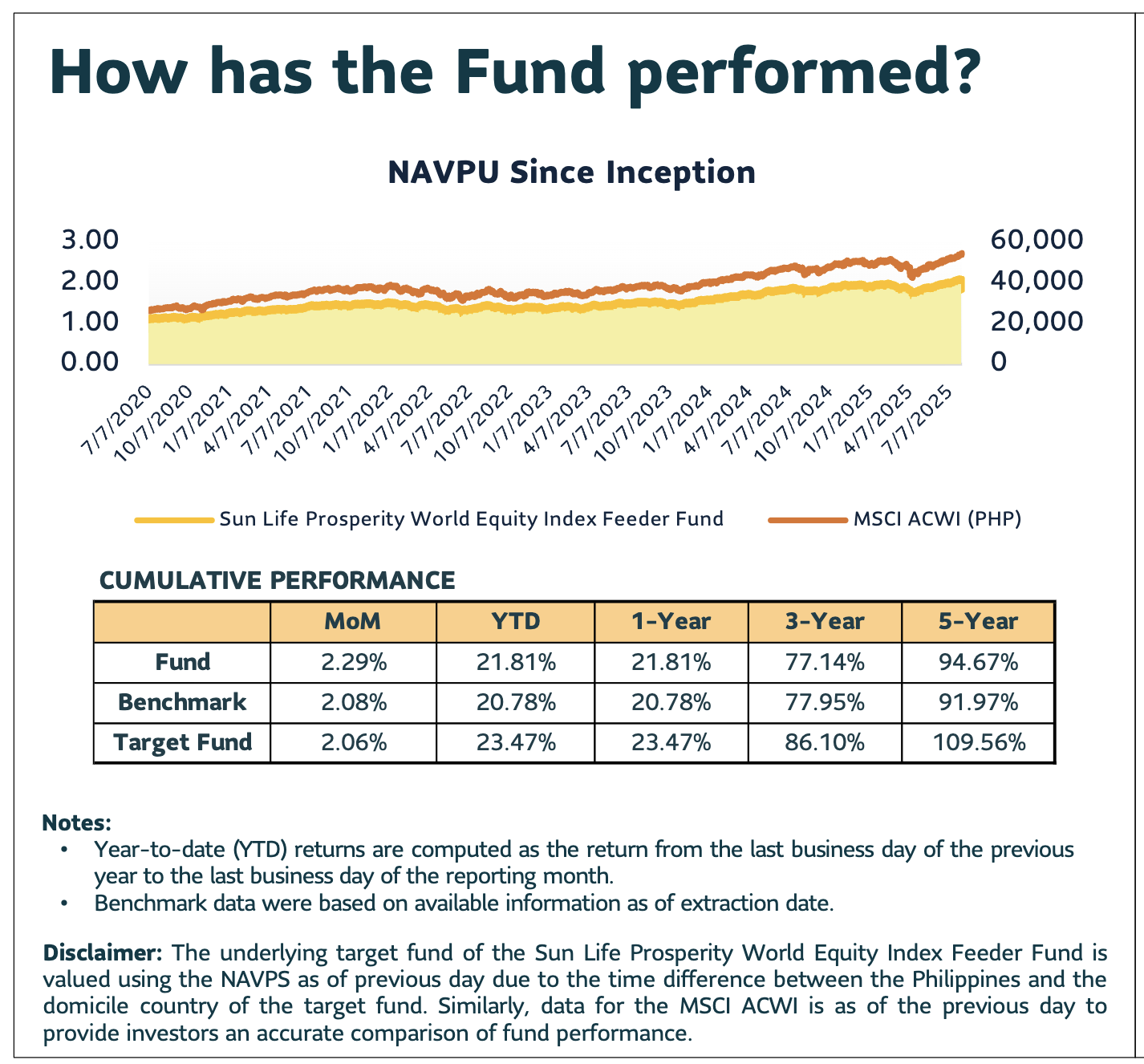

Instead of spending the recovered ₱60,000 annually, I redirected it into a global equity fund that invests in the SPDR MSCI All Country World Index UCITS ETF.

This ETF holds companies like:

• Nvidia

• Apple

• Microsoft

According to State Street Global Advisors, these are among its largest holdings.

Historical 5-year cumulative return: 94.67%

Net of approximately 1.15% annual management fees.

Let’s run a simplified projection.

If you invest ₱60,000 per year for 5 years:

Total capital invested:

₱300,000

If returns matched the historical 5-year cumulative rate:

Estimated value:

Approximately ₱520,000 to ₱580,000

If returns were cut in half, around 47% cumulative:

Estimated value:

Approximately ₱430,000 to ₱450,000

Even under moderate assumptions, redirected subscription money creates real capital growth.

Important tax note in the Philippines:

Gains from mutual funds are currently exempt from capital gains tax for individual investors under the TRAIN Law. There is no early redemption fee.

Redemption value equals:

Total units held × Current NAVPU.

That’s what hits your bank.

7. Why This Strategy Works

It does three things:

Breaks automation

Subscriptions are designed to be invisible.

Neutralizes sunk cost bias

You decide before paying, not after.

Introduces productive friction

Extra steps reduce impulse funding.

Finance is not about willpower.

It’s about system design.

Your One-Sentence Rule

Before you close this page, create one rule for yourself.

For example:

“I only keep subscriptions that return more value than they cost every month.”

Or:

“If I forget about it for 30 days, I cancel it.”

Write it down.

Because subscriptions are not the enemy.

Unexamined automation is.

If this helped you rethink how money quietly moves in your life, share it with someone who might need it.

Small leaks sink large ships.

And small corrections build real wealth.

About the Author

David Isaiah Angway is a Chartered Wealth Advisor, Estate Planner, and Strategic Financial Partner to high-net-worth individuals, affluent professionals, and legacy-focused families across the Philippines. With over ₱948 million in client risk portfolios under management, he guides clients through high-stakes decisions involving wealth structuring, succession, and multigenerational legacy.

With 13+ years of experience in financial services, David is known for his values-based approach, discretion, and deep expertise in estate planning and wealth preservation. His insights have been featured on TEDx, Bloomberg Philippines, ANC On the Money, Bilyonaryo News Channel, Moneysense Magazine, and BusinessMirror.

Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as financial, legal, or tax advice. Every high-net-worth individual or family has unique needs, goals, and risk exposures. Readers are strongly encouraged to consult their board of advisors—including a licensed financial planner, estate attorney, tax consultant, and relevant professionals—before making any financial decisions or implementing strategies discussed herein. Names and scenarios have been changed to protect privacy.

David Isaiah Angway assumes no liability for any loss, harm, or damages arising directly or indirectly from the use of this content. While every effort is made to ensure accuracy and relevance, no guarantees are made regarding the applicability of the information to your specific circumstances.

By reading this content, you agree that David Isaiah Angway is not responsible for any decisions you make based on this article.

© 2026 David Angway