VUL Fund Losing for Years? 27 Questions to Ask Before You Stay, Switch, or Rebalance

If your VUL fund has been underperforming, use this client checklist to review returns, benchmarks, fees, switching rules, currency risk, and conflicts of interest.

FINANCIAL STRATEGIES

David Isaiah Angway RFP

12/16/20254 min read

If your advisor keeps telling you to stay invested despite years of poor results, ask these questions for clear and accountable answers. Your goal is to get specific information, not just avoid disagreement.

Table of Contents

Tap to jump

Updated Jan 14, 2026

Performance and accountability

What are the fund’s returns over 1, 3, and 5 years after all fees, and where can I check these numbers?

What benchmark are we comparing the fund to, and how has it performed against it over the last 3 to 5 years?

Is the fund’s underperformance caused by the overall market, or is it specific to this fund? What proof do you have for your answer?

If we keep the investment, what recovery do you expect, and how much could I lose in a bad year?

Why are you recommending that I do nothing?

What is your main reason for telling me to stay, and what would have to change for you to suggest switching?

Are we waiting for a certain market event, price level, or time frame? Please give me a clear rule I can follow.

If the fund keeps underperforming for another year, what will we do, and what will make us take action?

How the fund fits your goals and timeline

Does the fund’s time frame match how long I plan to invest?

Did we agree on a conservative, moderate, or aggressive risk level, and does this fund still fit that choice?

If my main goal is protection, which part of my investment should be focused on stability?

Costs and other factors that might affect your advice

What fees in the VUL, like insurance, admin, and management charges, lower my fund’s value?

Are there any fees, limits on free switches, or costs when I switch funds?

If I switch funds, will it change my policy benefits, riders, or guarantees?

Are there any surrender, discontinuance, or penalty fees if I lower my premiums or withdraw everything?

Alternatives and suggested investment mix

If you suggest staying, what other options did you look at, and why did you decide against them?

If you recommend switching, what new investment mix do you suggest, and why?

How does your suggested mix lower the risk of being too focused on one market or sector?

If we move to global funds, what currency risks are there, and how will they affect my plan?

Practical steps and documentation

Can you show me, in pesos, what my fund value would be in three cases next year: if the market stays flat, recovers a bit, or goes down?

Can you give me your recommendation in writing, including the fund details, what would make us act, and when we’ll review again?

Checking for any conflicts of interest (asked politely)

Does keeping my money in this fund affect your pay or targets?

If I want a second opinion or decide to switch, will you help me with the paperwork and process?

FAQs

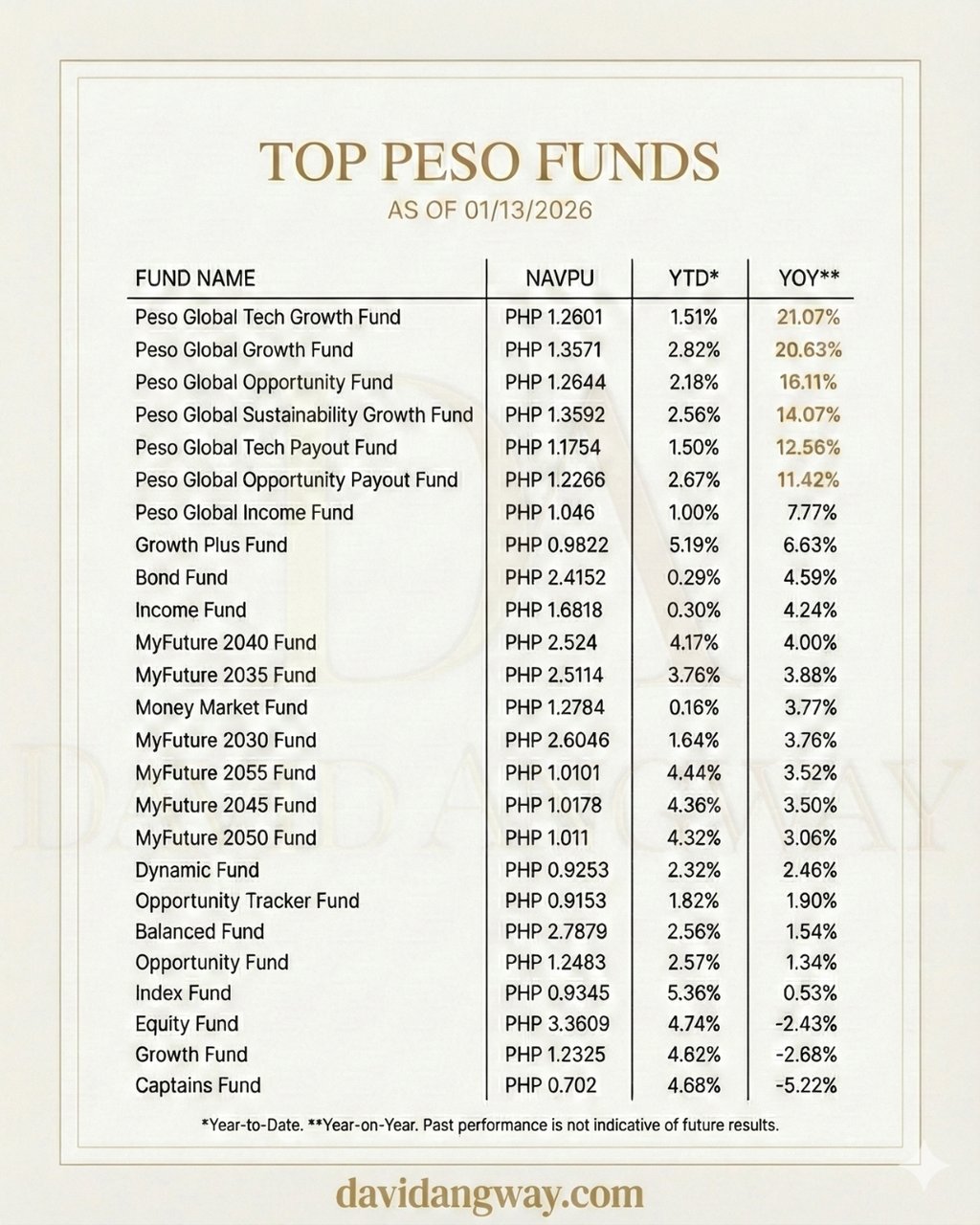

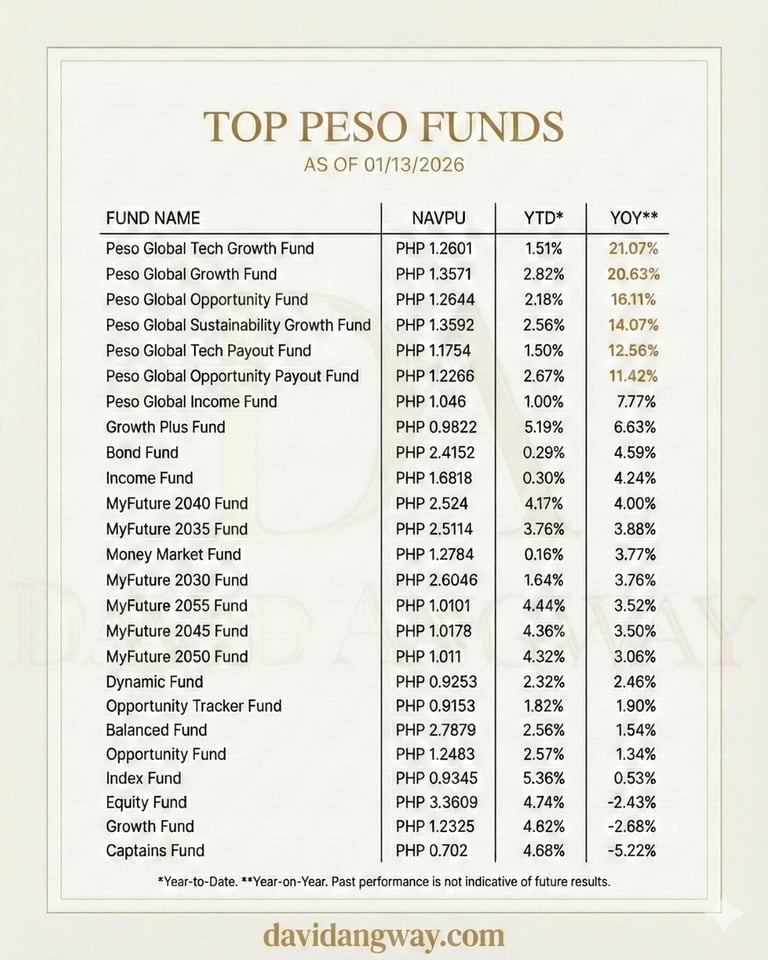

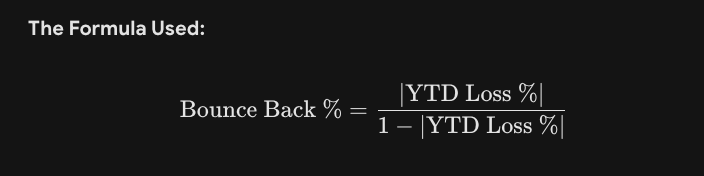

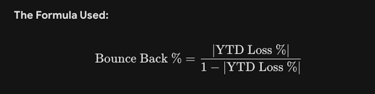

Q: Does the "Goal to bounce back" include my annual fees?

"A: No, the figures in the table focus strictly on market performance. They calculate the percentage gain needed to mathematically reverse the Year-to-Date loss.

In the real world, your investment also covers professional management and administrative costs each year. To fully break even in your account balance (net value), the fund’s growth will need to be slightly higher than the goal listed to account for these regular operating costs."

How did you end up with a computation?

The Verification Logic

When an investment loses value, the percentage gain required to return to the original value is always higher than the percentage lost. This is because you are growing from a smaller base amount.

Sample Checks

Here is the verification for three different funds from your list to prove the math holds up:

Captains Fund

YTD Loss: $11.14\%$ ($0.1114$)

Math: $0.1114 \div (1 - 0.1114) = 0.1114 \div 0.8886$

Result: $12.536\%$ (Rounded: 12.54%)

Verdict: Matches

Your next read: What Fund Managers Really Do in VUL and Mutual Funds

About the Author

David Isaiah Angway is a Chartered Wealth Advisor, Estate Planner, and Strategic Financial Partner to high-net-worth individuals, affluent professionals, and legacy-focused families across the Philippines. With over ₱948 million in client risk portfolios under management, he guides clients through high-stakes decisions involving wealth structuring, succession, and multigenerational legacy.

With 13+ years of experience in financial services, David is known for his values-based approach, discretion, and deep expertise in estate planning and wealth preservation. His insights have been featured on TEDx, Bloomberg Philippines, ANC On the Money, Bilyonaryo News Channel, Moneysense Magazine, and BusinessMirror.

Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as financial, legal, or tax advice. Every high-net-worth individual or family has unique needs, goals, and risk exposures. Readers are strongly encouraged to consult their board of advisors—including a licensed financial planner, estate attorney, tax consultant, and relevant professionals—before making any financial decisions or implementing strategies discussed herein. Names and scenarios have been changed to protect privacy.

David Isaiah Angway assumes no liability for any loss, harm, or damages arising directly or indirectly from the use of this content. While every effort is made to ensure accuracy and relevance, no guarantees are made regarding the applicability of the information to your specific circumstances.

By reading this content, you agree that David Isaiah Angway is not responsible for any decisions you make based on this article.

© 2026 David Angway